- Introduction

- Key Financial Ratios for Manufacturing Companies

- Interpretation of Ratios in the Manufacturing Industry

- Case Study: Applying Ratio Analysis to a Manufacturing Company

- Limitations of Ratio Analysis for Manufacturing Companies

- Best Practices for Effective Ratio Analysis in the Manufacturing Sector

- Conclusion

Introduction

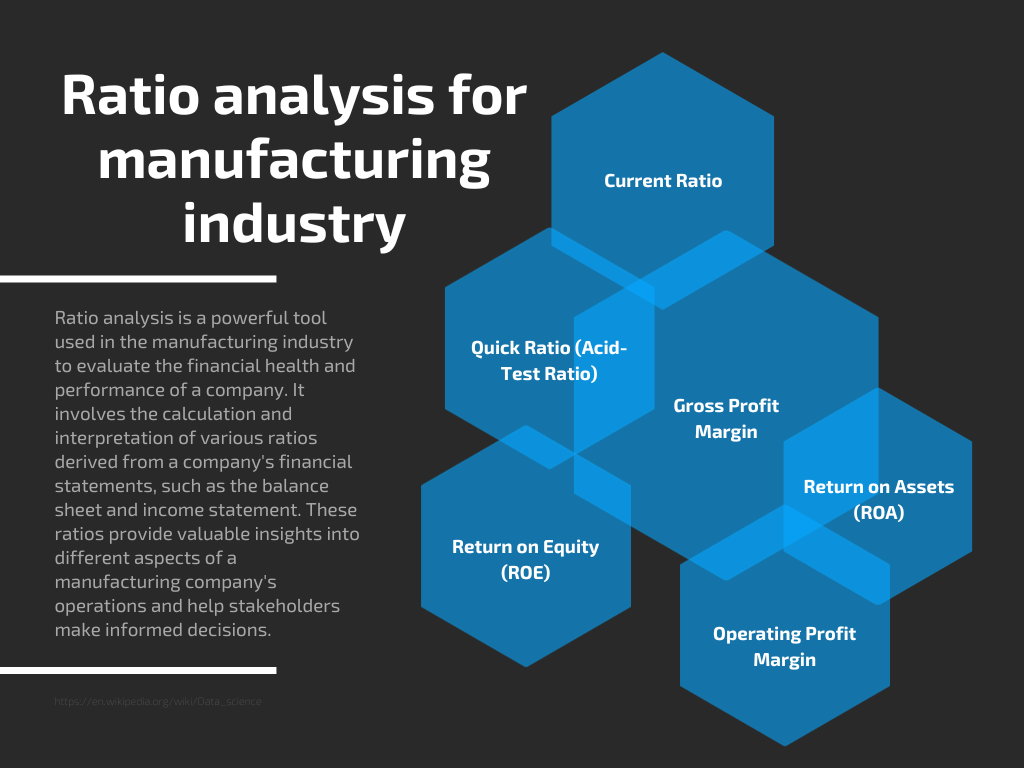

Ratio analysis is a powerful tool used in the manufacturing industry to evaluate the financial health and performance of a company. It involves the calculation and interpretation of various ratios derived from a company’s financial statements, such as the balance sheet and income statement. These ratios provide valuable insights into different aspects of a manufacturing company’s operations and help stakeholders make informed decisions.

One key aspect of ratio analysis is liquidity ratios, which assess a company’s ability to meet its short-term obligations. These ratios, including the current ratio and quick ratio, indicate the company’s ability to convert its assets into cash to cover immediate liabilities.

Profitability ratios are another crucial component of ratio analysis. These ratios, such as gross profit margin, operating profit margin, and net profit margin, reveal the company’s efficiency in generating profits from its manufacturing operations.

Additionally, leverage ratios measure a company’s debt levels and its capacity to meet long-term obligations. These ratios include the debt-to-equity ratio and interest coverage ratio, which provide insights into a manufacturing company’s financial stability and risk.

Key Financial Ratios for Manufacturing Companies

Liquidity Ratios

Liquidity ratios are a set of financial ratios used to assess a company’s ability to meet its short-term obligations. These ratios measure the company’s ability to convert its assets into cash quickly. The two commonly used liquidity ratios in the manufacturing industry are the current ratio and the quick ratio.

The current ratio is calculated by dividing current assets by current liabilities. It indicates whether a company has enough current assets to cover its current liabilities. A higher current ratio is generally preferred, as it suggests a stronger ability to meet short-term obligations.

The quick ratio, also known as the acid-test ratio, is a more stringent measure of liquidity. It excludes inventory from current assets, as inventory may not be easily convertible to cash. The quick ratio provides a more conservative assessment of a company’s ability to pay off its current liabilities.

These liquidity ratios help stakeholders assess a manufacturing company’s ability to manage its working capital effectively and ensure the availability of funds to meet its immediate financial obligations.

Efficiency Ratios

Efficiency ratios are financial metrics used to evaluate a company’s operational efficiency and effectiveness in utilizing its assets. In the manufacturing industry, efficiency ratios provide insights into how well a company is managing its resources and generating revenue. Two commonly used efficiency ratios in manufacturing are the inventory turnover ratio and the asset turnover ratio.

The inventory turnover ratio measures how quickly a company is selling and replacing its inventory. A higher ratio indicates efficient inventory management and sales.

The asset turnover ratio measures how efficiently a company utilizes its total assets to generate sales. A higher ratio suggests effective asset utilization and revenue generation.

By analyzing these efficiency ratios, stakeholders can assess a manufacturing company’s productivity, and effectiveness in utilizing resources, and identify areas for improvement in operational performance.

Profitability Ratios

Profitability ratios are financial metrics used to assess a company’s ability to generate profits from its operations. These ratios provide insights into a company’s profitability and its ability to generate a return on investment. In the manufacturing industry, profitability ratios are crucial indicators of financial performance.

Gross profit margin measures the percentage of sales revenue that remains after deducting the cost of goods sold. It indicates how effectively a company manages its production costs.

Operating profit margin measures the profitability of a company’s core operations by assessing the percentage of operating income generated from sales.

Net profit margin measures the overall profitability of a company by calculating the percentage of net income generated from sales after deducting all expenses.

These profitability ratios help stakeholders evaluate a manufacturing company’s profitability, efficiency in cost management, and overall financial performance. They are essential for making informed decisions regarding investments, pricing strategies, and cost control measures.

Solvency Ratios

Solvency ratios are financial metrics that assess a company’s long-term financial stability and its ability to meet its long-term debt obligations. These ratios are crucial in evaluating a manufacturing company’s financial health and its ability to withstand financial challenges. Two commonly used solvency ratios in the manufacturing industry are the debt-to-equity ratio and the interest coverage ratio.

The debt-to-equity ratio measures the proportion of debt-to-equity financing in a company’s capital structure. It indicates the level of financial risk and the extent to which a company relies on debt for funding its operations.

The interest coverage ratio assesses a company’s ability to meet its interest payments on outstanding debt. It measures the company’s earnings relative to its interest expenses, providing insights into its capacity to cover interest obligations.

Solvency ratios help stakeholders evaluate a manufacturing company’s long-term financial stability, risk exposure, and ability to repay its debts. These ratios are important for lenders, investors, and creditors when making decisions about providing financing or extending credit to the company.

Interpretation of Ratios in the Manufacturing Industry

Ratios and its significance

Current Ratio:

This ratio compares a company’s current assets to its current liabilities and indicates its ability to cover short-term obligations. A higher current ratio signifies better liquidity and suggests that the company can easily meet its short-term financial commitments.

Quick Ratio (Acid-Test Ratio):

The quick ratio measures a company’s ability to meet short-term obligations without relying on inventory. It excludes inventory from current assets as inventory may not be easily convertible to cash. A higher quick ratio indicates stronger liquidity and suggests that the company can quickly pay off its immediate liabilities.

Gross Profit Margin:

This ratio measures the profitability of a company’s manufacturing operations by comparing its gross profit to net sales. It reflects the company’s ability to generate profits after deducting the cost of goods sold. A higher gross profit margin signifies better cost control and efficient manufacturing processes.

Operating Profit Margin:

This ratio assesses the profitability of a company’s core operations by comparing operating income to net sales. It indicates the company’s ability to generate profits from its day-to-day manufacturing activities. A higher operating profit margin suggests strong operational efficiency and effective cost management.

Net Profit Margin:

The net profit margin measures the overall profitability of a company by comparing net income to net sales. It reflects the company’s ability to generate profits after accounting for all expenses, including taxes and interest. A higher net profit margin indicates better overall financial performance and effective management of costs and expenses.

Return on Assets (ROA):

This ratio evaluates a company’s ability to generate profits from its total assets. It compares net income to average total assets and indicates the efficiency of asset utilization. A higher ROA suggests better management of assets and higher profitability from the company’s investment in resources.

Return on Equity (ROE):

The ROE measures a company’s profitability concerning shareholders’ equity. It compares net income to average shareholders’ equity and indicates the return generated for shareholders’ investments. A higher ROE signifies efficient utilization of equity and higher returns for shareholders.

Comparison of ratios against industry benchmarks and historical data

Comparing financial ratios against industry benchmarks and historical data is essential to gain meaningful insights into a company’s performance. Industry benchmarks provide a standard for comparison, allowing stakeholders to assess how a company measures up against its peers. Historical data, on the other hand, enables the evaluation of a company’s performance over time and identifies trends and patterns.

By comparing ratios against industry benchmarks, stakeholders can identify areas of strength or weakness relative to the industry average. Comparing ratios to historical data helps assess the company’s progress, track performance trends, and identify areas of improvement or potential risks. This analysis aids in making informed decisions, setting realistic goals, and implementing strategies to enhance financial performance in the manufacturing industry.

Case Study: Applying Ratio Analysis to a Manufacturing Company

Case Study: Ratio Analysis for XYZ Manufacturing Company

XYZ Manufacturing Company is a well-established player in the manufacturing industry, specializing in the production of industrial machinery. The company’s management team is interested in assessing its financial performance and making informed decisions for future growth. They decide to conduct a thorough ratio analysis to gain insights into the company’s financial health and compare it against industry benchmarks and historical data.

Liquidity Ratios:

The current ratio for XYZ Manufacturing is calculated to be 2.5, indicating a strong ability to meet short-term obligations. This ratio is higher than the industry average of 2.0, highlighting the company’s excellent liquidity position. However, the quick ratio of 1.8 suggests that XYZ Manufacturing could improve its ability to meet short-term obligations without relying on inventory.

Profitability Ratios:

XYZ Manufacturing’s gross profit margin stands at 40%, exceeding the industry average of 35%. This indicates efficient cost management and competitive pricing strategies. The operating profit margin of 18% is lower than the industry average of 20%, signaling room for improvement in operational efficiency. The net profit margin of 12% is in line with the industry average, suggesting effective management of expenses.

Solvency Ratios:

The debt-to-equity ratio of 0.75 reveals that XYZ Manufacturing relies more on equity financing than debt. This is lower than the industry average of 1.0, indicating a conservative capital structure. The interest coverage ratio of 6 indicates that the company has sufficient earnings to cover its interest payments comfortably.

By comparing these ratios against industry benchmarks and historical data, XYZ Manufacturing can identify areas of strength and weakness. The company can leverage its strong liquidity position, focus on improving operational efficiency, and explore opportunities for enhancing profitability. With a conservative capital structure and comfortable interest coverage, XYZ Manufacturing can confidently plan for future growth and make informed financial decisions.

This case study demonstrates the practical application of ratio analysis in the manufacturing industry, providing valuable insights for strategic decision-making and enhancing financial performance.

Limitations of Ratio Analysis for Manufacturing Companies

While ratio analysis is a valuable tool for assessing the financial performance of manufacturing companies, it is important to acknowledge its limitations:

Industry Variations:

Ratios can vary significantly across different industries within the manufacturing sector. Therefore, it is crucial to compare ratios against industry-specific benchmarks to obtain meaningful insights. General benchmarks may not accurately reflect the unique characteristics and dynamics of a particular manufacturing industry segment.

Lack of Context:

Ratio analysis provides numerical insights but does not provide the full context behind the numbers. It is important to consider qualitative factors, such as market conditions, technological advancements, and industry-specific challenges, to interpret the ratios accurately.

Historical Data Limitation:

Relying solely on historical data for ratio analysis may not capture the dynamic nature of the manufacturing industry. Factors such as changing market trends, evolving customer preferences, and technological disruptions can significantly impact future performance, making historical ratios less reliable for future predictions.

Limited Focus:

Ratios offer a quantitative assessment of a company’s financial health but do not provide a comprehensive view of non-financial factors that may impact performance. Factors such as market share, product quality, innovation, and customer satisfaction are not captured by traditional financial ratios.

Manipulation and Window Dressing:

Companies can manipulate financial statements to present a more favorable picture of their performance, which can affect the accuracy and reliability of ratios. Window dressing techniques, such as timing inventory adjustments or deferring expenses, can distort the ratios and mislead stakeholders.

External Factors:

Ratio analysis does not consider external factors such as economic conditions, changes in government regulations, or industry disruptions. These factors can significantly impact a manufacturing company’s performance and may not be reflected in the ratios alone.

Best Practices for Effective Ratio Analysis in the Manufacturing Sector

Use Industry-Specific Benchmarks:

Comparing ratios against industry benchmarks provides context and enables a more accurate assessment of a manufacturing company’s performance. Utilize industry-specific benchmarks to gain insights into how the company fares against its peers and competitors.

Analyze Trend Analysis:

Instead of relying solely on a single year’s ratio values, analyze trends over multiple periods. Assessing the changes in ratios over time helps identify patterns and allows for a more comprehensive evaluation of the company’s financial performance.

Consider Non-Financial Factors:

While ratios provide quantitative insights, it is crucial to consider non-financial factors that impact a manufacturing company’s performance. Factors such as market conditions, technological advancements, competitive landscape, and customer preferences should be taken into account to interpret ratio analysis accurately.

Combine Ratios with Qualitative Analysis:

Ratio analysis should not be viewed in isolation. It should be combined with qualitative analysis, such as management discussions, industry reports, and market research, to gain a holistic understanding of the company’s operations, strategies, and prospects.

Focus on Key Ratios:

Instead of analyzing a large number of ratios, identify key ratios that are most relevant to the manufacturing sector. These may include liquidity ratios, profitability ratios, efficiency ratios, and solvency ratios. Concentrating on key ratios allows for a more focused and meaningful analysis.

Cross-Check with Other Financial Metrics:

Ratios should be cross-checked and complemented with other financial metrics, such as cash flow analysis, working capital management, and return on investment calculations. This helps in validating the findings and obtaining a more comprehensive view of the company’s financial health.

Be Aware of Limitations:

Understand the limitations of ratio analysis and its applicability to the manufacturing sector. Consider external factors, potential manipulations, and the need for qualitative analysis when interpreting the results.

Conclusion

In conclusion, ratio analysis is a valuable tool in the manufacturing industry for evaluating a company’s financial performance and making informed decisions. Liquidity ratios provide insights into a company’s ability to meet short-term obligations, while profitability ratios assess its ability to generate profits from manufacturing operations. Efficiency ratios help gauge operational effectiveness and asset utilization, while solvency ratios evaluate long-term financial stability.

By comparing ratios against industry benchmarks and historical data, stakeholders can identify areas of strength and weakness, set realistic goals, and implement strategies to enhance financial performance. It is important to consider the limitations of ratio analysis and complement it with qualitative analysis to gain a comprehensive understanding of a manufacturing company’s financial health.

Effective ratio analysis in the manufacturing sector involves using industry-specific benchmarks, analyzing trends, considering non-financial factors, and cross-checking with other financial metrics. By following best practices, stakeholders can leverage ratio analysis to assess liquidity, profitability, efficiency, and solvency, ultimately driving strategic decision-making and supporting the long-term success of manufacturing companies.