- Introduction to Manufacturing Financial Reporting

- Unlocking Prosperity: The Crucial Role of Accurate Financial Reporting in Manufacturing

- Decoding Manufacturing Financial Reports: Essential Components

- Cost Accounting Demystified: Illuminating Manufacturing Financial Strategies

- Inventory Valuation Insights: FIFO, LIFO, and Weighted Average Methods Unveiled

- Performance Metrics and KPIs for Manufacturing Financial Reporting

- Compliance and Regulations in Manufacturing Financial Reporting

- Technology and Tools for Streamlining Manufacturing Financial Reporting

- Top 6 Manufacturing accounting software – 2024

- Case Studies and Examples of Effective Manufacturing Financial Reporting

- Challenges and Future Trends in Manufacturing Financial Reporting

- Conclusion and Key Takeaways

Introduction to Manufacturing Financial Reporting

Step into the heart of Manufacturing Financial Reporting, where numbers and stories intertwine to shape the compelling tale of financial success. Picture a busy factory floor, machines dancing energetically, turning dreams into reality. In this lively world, Manufacturing Financial Reporting emerges as the quiet storyteller, translating the rhythmic buzz of production into a narrative of economic vitality.

The story begins with records, where each entry is a stroke, painting the picture of a company’s financial journey. From the start of raw materials to the peak of revenue, every number contributes to the plot. The characters are costs and profits, and the stage is the balance sheet. Join us as we embark on a journey through these financial pages, where the story of manufacturing unfolds – a tale of resilience, strategy, and prosperity, captured in the enchanting language of numbers.

Unlocking Prosperity: The Crucial Role of Accurate Financial Reporting in Manufacturing

Accurate financial reporting in manufacturing is the bedrock of informed decision-making and sustainable growth. Imagine a manufacturing facility as a complex puzzle, where every piece represents a financial transaction. Precision in financial reporting ensures that these pieces fit seamlessly, offering a clear and comprehensive picture of the company’s economic landscape.

Reliable financial data empowers manufacturers to assess the true cost of production, identify areas for cost-saving, and strategically allocate resources. It serves as a compass, guiding management through the dynamic terrain of market fluctuations and economic challenges. Additionally, accurate financial reporting enhances transparency and builds trust among stakeholders, fostering a healthy business ecosystem.

In the manufacturing realm, where efficiency and profitability are paramount, precise financial reporting acts as a cornerstone, enabling companies to navigate uncertainties and plot a course toward long-term success.

Decoding Manufacturing Financial Reports: Essential Components

Income Statements

Income statements, crucial in manufacturing financial reporting, encapsulate a company’s profitability over a specific period. Also known as profit and loss statements, they detail revenues, costs, and expenses, ultimately revealing net income or loss. In the manufacturing sector, income statements dissect operational efficiency by delineating the cost of goods sold (COGS), gross profit margins, and operating expenses.

These essential documents aid decision-makers in evaluating the business’s financial performance, identifying areas for improvement, and making strategic adjustments. By providing a snapshot of revenue generation and expenditure, income statements are invaluable tools for assessing the overall fiscal health and sustainability of manufacturing enterprises.

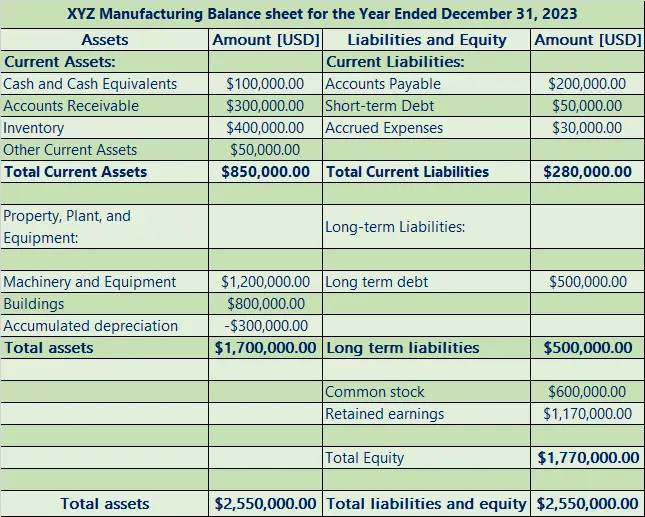

Balance Sheets

Balance sheets are vital components of financial reporting in manufacturing, offering a snapshot of a company’s financial position at a specific point in time. These documents present the equation of assets equaling liabilities and equity. In the manufacturing sector, assets encompass tangible resources like machinery and inventory, while liabilities include debts and obligations.

Equity reflects the ownership stake. The balance sheet guides stakeholders in assessing the company’s liquidity, solvency, and overall financial health. By delineating the relationship between assets and obligations, balance sheets empower decision-makers in strategic planning and resource allocation, ensuring a firm foundation for sustained growth and stability.

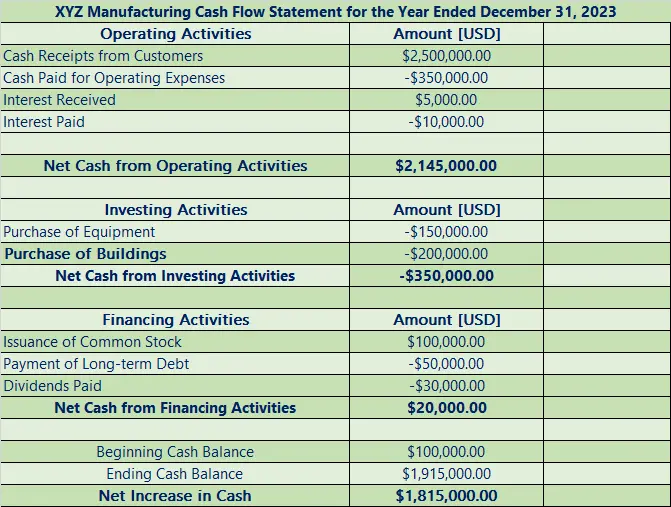

Cash Flow Statements

Cash flow statements in manufacturing are vital financial tools, offering insights into the movement of funds within a company. These statements track the sources and uses of cash, detailing operational, investing, and financing activities. For manufacturing entities, cash flow statements illuminate the cash generated or consumed during the production process, capital expenditures on machinery or facilities, and financing activities such as loans or dividends.

By providing a holistic view of a company’s liquidity, cash flow statements guide decision-makers in managing working capital effectively, ensuring financial stability, and making informed choices for sustained growth and profitability in the dynamic manufacturing landscape.

Cost Accounting Demystified: Illuminating Manufacturing Financial Strategies

Cost accounting in manufacturing involves tracking and analyzing all costs associated with producing goods. It helps businesses determine the true cost of each product, facilitating informed decision-making. For instance, in a manufacturing process, direct costs like raw materials and labor, as well as indirect costs such as factory overhead, are considered.

Imagine a bicycle manufacturer: the cost accounting process would include not just the materials and labor to build each bike but also the share of utility bills and equipment depreciation attributable to the production. This comprehensive approach aids in pricing strategies, cost control, and optimizing overall production efficiency.

Direct vs. Indirect Costs: Strategic Cost Analysis in Manufacturing

Direct costs are expenses directly tied to producing a specific product or service, like raw materials and labor. Indirect costs are not directly traceable to a product but contribute to overall operations, such as utilities or administrative salaries. Distinguishing these helps businesses analyze and allocate costs accurately for better financial management.

Consider a bakery: the cost of flour and the wages of bakers are direct costs, directly linked to making bread. On the other hand, the electricity bill for the entire bakery, benefiting all products, is an indirect cost. While direct costs are specific to each loaf of bread, indirect costs contribute to the overall functioning of the bakery without a direct tie to a single product.

Variable vs. Fixed Costs: Shaping Financial Landscapes in Manufacturing

Variable costs change with production levels, like raw materials or hourly wages. Fixed costs remain constant regardless of production, such as rent or salaries. Variable costs fluctuate with business activity, while fixed costs persist, contributing to the total cost structure irrespective of output variations.

Consider a car manufacturing plant: the cost of steel, which varies with the number of cars produced, is variable. In contrast, the monthly lease payment for the manufacturing facility remains fixed, unaffected by the number of cars manufactured. Variable costs change with production volume, while fixed costs persist, providing a clear distinction in cost behavior.

Overhead Allocation Methods: Precision in Distributing Manufacturing Costs

Overhead allocation methods play a crucial role in distributing indirect costs across various products or services. Imagine you manage a furniture workshop where you produce tables and chairs. To allocate the rent expense, you might use the machine hours method. If tables require more machine hours than chairs for production, they would bear a larger share of the rent.

Conversely, the number of setups method might allocate maintenance costs based on the frequency of equipment setups. If chairs involve more setup changes, they absorb a higher portion of the maintenance costs. These methods help ensure that each product bears a fair share of the indirect costs, providing a more accurate representation of the true cost of production for informed decision-making.

Inventory Valuation Insights: FIFO, LIFO, and Weighted Average Methods Unveiled

In the realm of manufacturing financial reporting, inventory valuation is a pivotal component that shapes a company’s financial landscape. It involves assigning values to goods held for production or sale, influencing financial statements, and strategic decision-making.

Proper inventory valuation methods, like FIFO (First In, First Out) or LIFO (Last In, First Out), impact a manufacturer’s reported profits and tax liabilities. Accurate reporting ensures a true reflection of a company’s financial health, aiding in resource allocation and investor confidence. Navigating the intricacies of inventory valuation is essential for manufacturing entities seeking transparent and reliable financial reporting.

FIFO, LIFO, and Weighted Average Methods

In the realm of Manufacturing Financial Reporting, three key inventory valuation methods—FIFO (First In, First Out), LIFO (Last In, First Out), and Weighted Average—play a significant role in shaping a company’s financial landscape.

FIFO involves valuing inventory based on the assumption that the first items purchased are the first ones sold.

Imagine a bakery; if the first batch of flour costs $5, and the next costs $6, FIFO would assign the cost of goods sold at $5 until that batch is exhausted.

Conversely, LIFO assumes the last items purchased are the first ones sold. Using the same bakery example, under LIFO, the cost of goods sold would be based on the most recent batch’s price, impacting profit margins and tax liabilities.

The Weighted Average method calculates the average cost of all units. For instance, if a manufacturer produces chairs with varying production costs, the Weighted Average method provides a blended cost for each unit.

These methods, crucial in Manufacturing Financial Reporting, influence reported profits, tax obligations, and the overall financial health of a business. Selecting the appropriate method requires a nuanced understanding of a company’s operations and financial objectives.

Just-in-Time (JIT) Inventory Systems

Just-in-Time (JIT) inventory systems revolutionize manufacturing by optimizing efficiency and minimizing excess inventory. In JIT, products are produced only as needed, eliminating surplus stockpiles. Picture a car manufacturer ordering precisely the required number of components for immediate assembly, avoiding storage costs and waste.

JIT relies on synchronized processes, ensuring materials arrive precisely when needed, reducing holding costs, and enhancing cash flow. However, this system demands meticulous coordination to avert disruptions. Imagine a smartphone assembly line where components arrive just in time for immediate integration, minimizing storage expenses and streamlining production, epitomizing the efficiency hallmark of JIT inventory systems.

Performance Metrics and KPIs for Manufacturing Financial Reporting

In the realm of manufacturing, tracking performance metrics and Key Performance Indicators (KPIs) is paramount for informed decision-making and financial success. These metrics provide a comprehensive view of a company’s operational health, financial stability, and overall efficiency. For manufacturing entities, effective performance measurement aligns with their financial reporting strategies.

Robust Manufacturing Financial Reporting relies heavily on identifying and analyzing KPIs, allowing businesses to assess profitability, cost-effectiveness, and operational excellence. As manufacturing processes evolve, the strategic implementation of performance metrics becomes integral, offering insights that shape financial strategies and contribute to the long-term sustainability of manufacturing ventures.

OEE (Overall Equipment Effectiveness)

Overall Equipment Effectiveness (OEE) stands as a pivotal metric in manufacturing, evaluating the efficiency of equipment utilization. It encompasses three key factors: availability, performance, and quality. Calculating OEE offers insights into the effectiveness of production processes, directly impacting Manufacturing Financial Reporting.

By identifying and mitigating downtime, improving production rates, and ensuring quality output, OEE contributes to cost optimization and enhances the financial performance of manufacturing operations. In the context of Manufacturing Financial Reporting, OEE serves as a crucial indicator of operational excellence and resource utilization.

Throughput Yield

Throughput Yield is a vital metric in manufacturing, assessing the proportion of defect-free units produced in a process. It focuses on the overall efficiency of the production line, measuring the yield of acceptable products. As a key performance indicator in manufacturing, Throughput Yield influences the quality aspect of Manufacturing Financial Reporting.

By minimizing defects and enhancing production reliability, this metric directly contributes to cost savings, revenue improvement, and overall financial success, aligning with the broader objectives of Manufacturing Financial Reporting.

Cycle Time and Lead Time

Cycle Time and Lead Time are critical metrics in manufacturing, evaluating the efficiency of production processes. Cycle Time measures the time required to complete a specific task, while Lead Time encompasses the total time from order placement to product delivery.

These metrics directly impact operational efficiency and, consequently, Manufacturing Financial Reporting. By minimizing cycle and lead times, manufacturers enhance productivity, reduce costs, and optimize resource allocation, contributing to improved financial performance and aligning with the goals of Manufacturing Financial Reporting.

Compliance and Regulations in Manufacturing Financial Reporting

In the landscape of manufacturing, adherence to compliance and regulations is integral for sound financial practices and ethical governance. Manufacturers must navigate a complex web of industry-specific standards, legal requirements, and financial reporting regulations. Ensuring compliance is not just a legal obligation but a cornerstone of transparent and accurate Manufacturing Financial Reporting.

Straying from compliance may lead to legal consequences and financial penalties. Moreover, robust compliance practices foster trust among stakeholders, positively impacting a company’s reputation. Navigating the intricate terrain of compliance and regulations is indispensable for manufacturers committed to maintaining financial integrity and fostering confidence in Manufacturing Financial Reporting.

GAAP (Generally Accepted Accounting Principles)

GAAP, or Generally Accepted Accounting Principles, provides a standardized framework for financial reporting across industries, including Manufacturing Financial Reporting. These principles guide the recording, presentation, and disclosure of financial information, ensuring consistency and transparency.

Manufacturers adhere to GAAP to communicate their financial health accurately, fostering trust among stakeholders. By aligning with GAAP, manufacturers enhance the credibility of their financial statements, supporting informed decision-making and contributing to the reliability and integrity of Manufacturing Financial Reporting.

IFRS (International Financial Reporting Standards)

IFRS (International Financial Reporting Standards) serves as a globally recognized framework for financial reporting, fostering transparency and comparability. For manufacturers, adherence to IFRS is crucial in ensuring standardized and coherent financial statements. Embracing IFRS principles in Manufacturing Financial Reporting enhances the credibility of financial information, streamlines cross-border business transactions, and facilitates better decision-making.

As manufacturers operate in a diverse global market, aligning with IFRS ensures consistency, providing stakeholders with reliable insights into the financial performance of manufacturing entities across international landscapes.

Technology and Tools for Streamlining Manufacturing Financial Reporting

Embracing technology and advanced tools has become imperative for streamlining Manufacturing Financial Reporting processes. In an era of rapid technological evolution, manufacturers are leveraging innovative solutions to enhance accuracy, efficiency, and real-time reporting. These technological advancements, specifically tailored for Manufacturing Financial Reporting, enable seamless data integration, automated analysis, and comprehensive insights.

Such tools not only optimize financial workflows but also ensure compliance with evolving reporting standards. Incorporating cutting-edge technology aligns manufacturing entities with modern financial reporting practices, fostering precision and agility in managing financial data for more informed decision-making.

ERP (Enterprise Resource Planning) Systems

Enterprise Resource Planning (ERP) systems have emerged as integral tools in manufacturing, revolutionizing operations and streamlining processes. Tailored for Manufacturing Financial Reporting, ERP systems seamlessly integrate various business functions, providing a centralized platform for data management.

From production and inventory to finance and human resources, these systems enhance efficiency, data accuracy, and decision-making capabilities. Manufacturers deploying ERP systems gain a comprehensive view of their financial landscape, contributing to more precise Manufacturing Financial Reporting and overall operational excellence.

Business Intelligence and Data Analytics

In the contemporary business landscape, Business Intelligence (BI) and Data Analytics have emerged as transformative forces, providing invaluable insights from vast datasets. BI involves gathering, analyzing, and visualizing data to inform strategic decision-making.

Data Analytics delves deeper, employing statistical techniques and predictive modeling to extract actionable insights. Together, they empower businesses to make informed choices, optimize processes, and uncover trends. In an era driven by data, the synergy of Business Intelligence and Data Analytics plays a pivotal role in shaping agile and competitive business strategies.

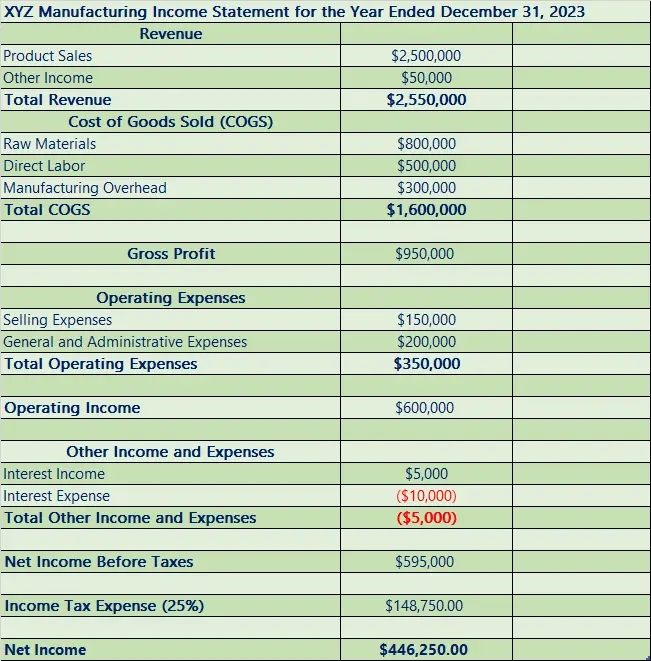

Case Studies and Examples of Effective Manufacturing Financial Reporting

In a notable case of effective Manufacturing Financial Reporting, XYZ Manufacturing implemented strategic changes to optimize its financial processes. Facing challenges in cost visibility and decision-making, the company adopted advanced ERP systems tailored for Manufacturing Financial Reporting. This integration enabled real-time tracking of production costs, enhanced inventory management, and streamlined reporting.

As a result, the accuracy of financial statements improved significantly. Additionally, the implementation led to a 20% reduction in operating costs within the first year. The newfound transparency facilitated better resource allocation and strategic planning.

Furthermore, XYZ Manufacturing utilized performance metrics aligned with Manufacturing Financial Reporting principles. By incorporating Key Performance Indicators (KPIs) such as Overall Equipment Effectiveness (OEE) and Throughput Yield, the company gained insights into operational efficiency and product quality. This proactive approach not only optimized production processes but also positively impacted financial outcomes.

These changes were instrumental in enhancing stakeholder confidence and attracting new investors. The refined Manufacturing Financial Reporting practices positioned XYZ Manufacturing as an industry leader committed to financial transparency and efficiency.

This case exemplifies how embracing advanced technology and aligning with Manufacturing Financial Reporting standards can drive operational excellence and financial success in the manufacturing sector.

Challenges and Future Trends in Manufacturing Financial Reporting

Manufacturing Financial Reporting encounters several challenges and anticipates transformative trends as industries evolve. One persistent challenge is the complexity of supply chains, making accurate financial reporting intricate. Balancing global compliance standards is another hurdle, as manufacturers often operate across diverse regulatory environments.

Moreover, the rise of Industry 4.0 introduces transformative trends. Integration of IoT devices and smart manufacturing technologies generates an influx of real-time data, challenging traditional reporting methodologies. However, embracing these technologies also presents an opportunity. Advanced analytics and machine learning are anticipated to revolutionize Manufacturing Financial Reporting, providing deeper insights and predictive capabilities.

The future of Manufacturing Financial Reporting also hinges on sustainability reporting. With an increasing focus on environmental, social, and governance (ESG) criteria, manufacturers are expected to integrate sustainability metrics into their financial reports. This dual focus on financial and sustainability reporting aligns with global initiatives for responsible and transparent business practices.

In conclusion, the challenges faced by Manufacturing Financial Reporting are met with promising trends. Adapting to Industry 4.0 technologies, incorporating advanced analytics, and integrating sustainability metrics reflect the trajectory of future practices. Navigating these challenges and embracing transformative trends positions manufacturing entities to not only meet compliance standards but also to thrive in an era that demands transparency, efficiency, and sustainable business practices in Manufacturing Financial Reporting.

Conclusion and Key Takeaways

- Manufacturing Financial Reporting as a Storyteller: Manufacturing Financial Reporting serves as the silent narrator in the dynamic world of manufacturing, translating the rhythmic buzz of production into a compelling tale of economic vitality.

- Importance of Accurate Financial Reporting: Precision in financial reporting is the cornerstone of informed decision-making and sustainable growth. It paints a comprehensive picture of a company’s economic landscape, guiding strategic planning and resource allocation.

- Key Components of Financial Reports: Income statements dissect operational efficiency, balance sheets provide a snapshot of financial position, and cash flow statements illuminate fund movement. Each plays a crucial role in assessing the fiscal health and sustainability of manufacturing entities.

- Cost Accounting and Decision-Making: Cost accounting aids in determining the true cost of each product, facilitating pricing strategies, cost control, and overall production efficiency.

- Inventory Valuation Methods: Proper inventory valuation, using methods like FIFO, LIFO, or Weighted Average, influences reported profits and tax liabilities, ensuring transparent and reliable financial reporting.

- Performance Metrics and KPIs: Tracking metrics like OEE, Throughput Yield, and cycle times provide a comprehensive view of operational health, aiding in assessing profitability, cost-effectiveness, and overall efficiency.

- Compliance and Reporting Standards: Adherence to GAAP and IFRS ensures standardized and coherent financial statements, fostering transparency and comparability in Manufacturing Financial Reporting.

- Embracing Technology for Efficiency: Utilizing ERP systems, Business Intelligence, and Data Analytics enhances accuracy, efficiency, and real-time reporting, aligning manufacturing entities with modern financial reporting practices.

Wow, wonderful weblog format! How lengthy have you ever been blogging for?

you made running a blog look easy. The full glance of

your web site is magnificent, as smartly as the content! You

can see similar: najlepszy sklep and here sklep internetowy