- Manufacturing accounting explained

- Optimizing Manufacturing Accounting for Success

- The Power of Manufacturing Accounting Systems

- Areas of manufacturing accounting

- Manufacturing Accounting Process Flow

- How to Establish a Manufacturing Accounting System

- Accounting software for Manufacturing

- Unlocking the Significance of Manufacturing Accounting

- Practical example for manufacturing accounting

- Limitations of manufacturing accounting

Manufacturing accounting explained

Manufacturing accounting is a specialized field crucial for managing the financial aspects of manufacturing companies. Its primary focus lies in accurately capturing and analyzing the costs associated with producing goods. The process begins by meticulously tracking direct costs, such as raw materials, labor, and production-related overhead expenses. This detailed breakdown ensures informed decision-making regarding pricing strategies, production efficiency, and overall profitability.

A fundamental concept in manufacturing accounting is the distinction between variable and fixed costs. Variable costs, like raw materials and direct labor, fluctuate with production levels, while fixed costs, such as rent and salaries, remain constant irrespective of production volume. Properly managing these costs is essential to determine the actual cost of goods sold and to establish competitive pricing.

Manufacturing accounting relies on key performance metrics, including the cost of goods manufactured (COGM) and the cost of goods sold (COGS). These metrics serve as valuable tools for assessing operational efficiency, identifying areas for cost reduction, and enhancing overall financial performance. In essence, manufacturing accounting provides businesses with essential financial insights, enabling them to optimize operations and achieve sustained success in the competitive manufacturing landscape.

Optimizing Manufacturing Accounting for Success

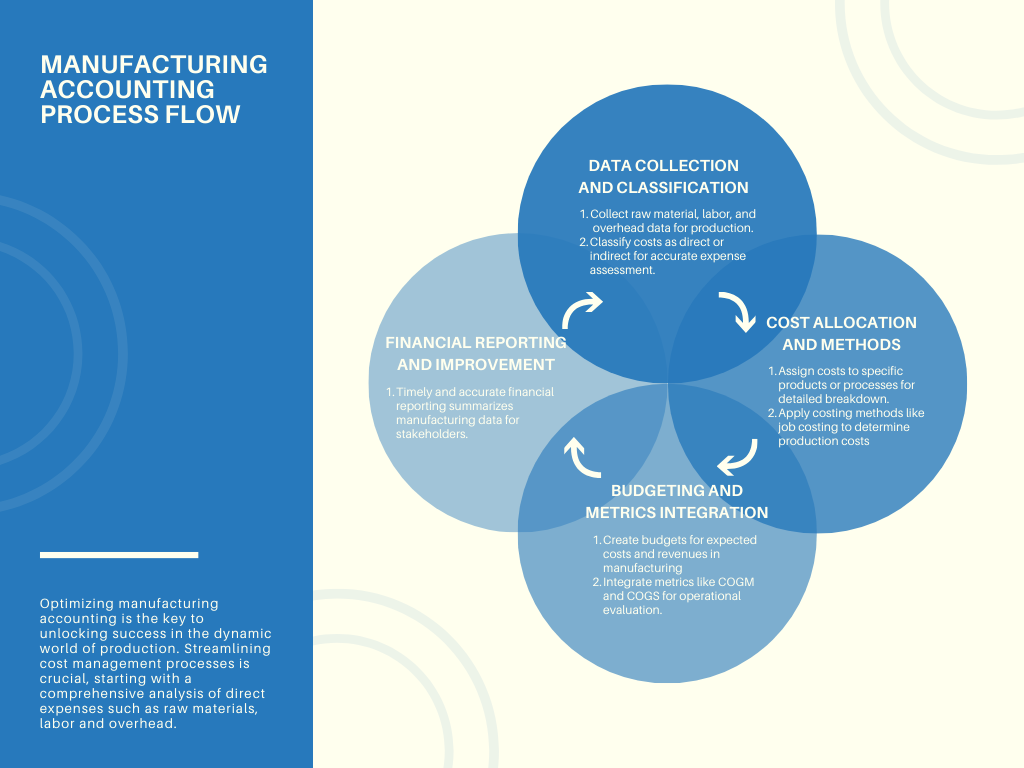

Optimizing manufacturing accounting is the key to unlocking success in the dynamic world of production. Streamlining cost management processes is crucial, starting with a comprehensive analysis of direct expenses such as raw materials, labor and overhead. By embracing efficiency in cost tracking, businesses gain the ability to make informed decisions, enhancing overall financial health.

Effective management of variable and fixed costs is paramount. Variable costs, responsive to production levels, demand vigilant monitoring for cost-effective outcomes. Fixed costs, unwavering in the face of production fluctuations, require strategic planning to ensure stability. A balanced approach to these cost categories is instrumental in determining the true cost of goods sold, allowing companies to set competitive prices and maintain profitability.

Integrating key performance metrics like the cost of goods manufactured (COGM) and the cost of goods sold (COGS) is the next step toward success. These metrics act as compasses, guiding businesses to operational efficiency and identifying opportunities for cost reduction. Harnessing the power of manufacturing accounting metrics provides a roadmap for sustained success, offering invaluable insights into operations and financial performance.

The Power of Manufacturing Accounting Systems

- Precision in Cost Tracking: Manufacturing accounting systems wield precision in tracking costs, from raw materials to overhead expenses. This precision ensures accurate insights into the production process, aiding informed decision-making.

- Efficient Resource Allocation: These systems facilitate the efficient allocation of resources by distinguishing between variable and fixed costs. By understanding cost dynamics, businesses can allocate resources strategically, optimizing production and enhancing profitability.

- Strategic Pricing: Manufacturing accounting systems empower businesses to set strategic prices. Accurate cost data enables companies to determine the true cost of goods sold, ensuring competitive pricing strategies that reflect both market dynamics and internal financial goals.

- Operational Insights: Key performance metrics, such as the cost of goods manufactured (COGM) and the cost of goods sold (COGS), provide operational insights. Businesses can identify areas for improvement, enhance efficiency, and implement targeted cost-reduction measures.

- Facilitating Compliance: Manufacturing accounting systems aid in compliance with regulatory requirements. They ensure that financial records align with industry standards, reducing the risk of errors and facilitating a smooth audit process.

Areas of manufacturing accounting

- Costing Methods: Manufacturing accounting utilizes various costing methods, including job costing, process costing, and activity-based costing. These methods enable precise allocation of costs, providing insights into specific expenses associated with individual products or production processes.

- Budgeting and Forecasting: In manufacturing accounting, the focus on budgeting involves creating financial plans based on expected costs and revenues. This proactive approach aids in resource allocation, and goal setting, and provides a benchmark for measuring actual performance against planned targets.

- Inventory Valuation: Manufacturing accountants actively engage in inventory valuation to ensure that financial statements accurately reflect the value of goods on hand. This is crucial for determining the cost of goods sold, assessing overall asset value, and maintaining financial transparency.

- Performance Measurement: Manufacturing accounting systems incorporate the development and analysis of performance metrics. These metrics evaluate the efficiency of production processes, workforce productivity, and overall financial health, allowing companies to identify areas for improvement and optimization.

- Financial Reporting: Timely and accurate financial reporting stands as a cornerstone of manufacturing accounting. This encompasses the preparation of financial statements, income statements, and balance sheets, providing stakeholders with a comprehensive view of the company’s financial performance and aiding in strategic decision-making.

- Variance Analysis: Manufacturing accountants conduct variance analysis to compare actual performance against budgeted or standard costs. This helps identify deviations, enabling businesses to understand the reasons behind discrepancies and take corrective actions.

- Cash Flow Management: Manufacturing accounting is instrumental in managing cash flow by tracking inflows and outflows. This ensures that the company has sufficient liquidity to meet operational needs, invest in growth opportunities, and handle unforeseen challenges.

Manufacturing Accounting Process Flow

- Data Collection: The process begins with the collection of data related to raw materials, labor, and overhead expenses incurred during production.

- Cost Classification: Manufacturing accountants classify costs into direct and indirect categories, distinguishing between those directly tied to production and those indirectly contributing to overall expenses.

- Cost Allocation: The allocated costs are then assigned to specific products or production processes, providing a detailed breakdown of expenses associated with each.

- Costing Methods Application: Various costing methods, such as job costing or process costing, are applied to determine the cost of producing goods with precision.

- Budgeting: Manufacturing accounting involves creating budgets that outline expected costs and revenues, providing a financial roadmap for the upcoming period.

- Performance Metrics Integration: Key performance metrics like the cost of goods manufactured (COGM) and the cost of goods sold (COGS) are integrated to evaluate operational efficiency and financial performance.

- Financial Reporting: Timely and accurate financial reporting, including income statements and balance sheets, summarizes the manufacturing accounting data for stakeholders.

- Analysis and Continuous Improvement: The final step involves analyzing the data, identifying variances, and implementing continuous improvement measures to enhance efficiency and reduce costs.

How to Establish a Manufacturing Accounting System

- Needs Assessment: Begin by conducting a thorough assessment of your manufacturing operation’s financial needs, considering factors such as the volume of production, types of products, and specific cost-tracking requirements.

- Select Appropriate Software: Choose a robust manufacturing accounting software that aligns with your business needs. Look for features that support cost tracking, inventory management, and financial reporting.

- Chart of Accounts Setup: Develop a comprehensive chart of accounts tailored to your manufacturing processes. This includes categorizing costs to provide a detailed breakdown of expenses.

- Implement Costing Methods: Choose and implement suitable costing methods, such as job costing or process costing, based on your production structure. Ensure consistency and accuracy in applying these methods.

- Training and Integration: Train your team on the new accounting system and integrate it seamlessly into your daily operations. This ensures that everyone understands the processes and can contribute to accurate data entry.

- Budgeting and Forecasting: Establish a budgeting process that aligns with your manufacturing goals. Create forecasts based on expected costs and revenues to guide financial planning.

- Regular Monitoring and Adjustments: Continuously monitor the system’s performance, making adjustments as needed. Regularly review financial reports to identify areas for improvement and efficiency gains.

- Compliance and Auditing: Ensure that your manufacturing accounting system complies with relevant regulations. Regularly conduct internal audits to verify accuracy and identify any potential areas of non-compliance or improvement.

Accounting software for Manufacturing

Selecting the right accounting software is crucial for manufacturing businesses. Renowned systems like SAP Business One offer comprehensive solutions, integrating financial processes with inventory and production management. QuickBooks Enterprise provides scalability and customizable features for manufacturing-specific needs.

Another notable option is Microsoft Dynamics 365 Finance and Operations, offering end-to-end visibility into financial and operational data. These software solutions streamline cost tracking, inventory valuation, and financial reporting, enhancing efficiency and accuracy in manufacturing accounting processes.

Unlocking the Significance of Manufacturing Accounting

Manufacturing accounting holds paramount significance in the business landscape, serving as the financial compass for production-oriented enterprises. By meticulously tracking costs associated with raw materials, labor, and overhead expenses, manufacturing accountants provide essential insights for strategic decision-making. The detailed breakdown of costs enables businesses to set competitive prices, optimize production efficiency, and ensure sustained profitability.

Furthermore, manufacturing accounting plays a pivotal role in fostering operational transparency and accountability. Through key performance metrics like the cost of goods manufactured (COGM) and the cost of goods sold (COGS), businesses gain a clear understanding of their financial health and operational efficiency.

This information empowers companies to identify areas for improvement, implement cost-saving measures, and make informed investments, ultimately contributing to the long-term success and resilience of manufacturing enterprises in today’s dynamic and competitive markets.

Practical example for manufacturing accounting

Consider XYZ Manufacturing, a company specializing in electronic components. In their manufacturing accounting:

- Cost Breakdown: XYZ accurately tracks costs, including $150,000 for raw materials, $75,000 in direct labor, and $30,000 in overhead for a specific production run.

- Cost Allocation: Applying activity-based costing, XYZ allocates overhead costs based on machine hours. For a production run of 10,000 units, each unit incurs $3 in overhead costs.

- COGM Calculation: The Cost of Goods Manufactured (COGM) is determined by summing direct materials, direct labor, and allocated overhead. For XYZ, COGM for the production run amounts to $255,000.

- COGS Determination: If 8,000 units are sold during the period, the Cost of Goods Sold (COGS) is $204,000 (8,000 units * $25.50 per unit).

- Gross Profit Analysis: With total revenue of $300,000 from sales, XYZ’s gross profit is $96,000 ($300,000 – $204,000), reflecting the profitability of its manufacturing operations.

COGM Calculation:

| Cost Component | Amount |

|---|---|

| Direct Materials | $150,000 |

| Direct Labor | $75,000 |

| Allocated Overhead | $30,000 |

| Total COGM | $255,000 |

COGS Determination

| Units Sold | COGS per Unit | Total COGS |

|---|---|---|

| 8,000 | $25.50 | $204,000 |

Gross Profit Analysis:

| Total Revenue | Total COGS | Gross Profit |

|---|---|---|

| $300,000 | $204,000 | $96,000 |

Limitations of manufacturing accounting

- Overhead Allocation Challenges: One limitation of manufacturing accounting lies in the allocation of overhead costs. Determining a fair and accurate method for assigning these costs to products can be complex, leading to potential distortions in cost calculations.

- Inflexibility in Changing Processes: Manufacturing accounting systems may face challenges adapting to changes in production processes. Rapid technological advancements or shifts in manufacturing methods can make it difficult to update accounting systems accordingly.

- Neglect of Non-Financial Factors: Manufacturing accounting tends to focus primarily on financial metrics, often neglecting non-financial factors crucial to a company’s overall performance, such as product quality, customer satisfaction, and employee productivity.

- Dependence on Historical Data: The reliance on historical data for cost calculations can be limiting. In rapidly changing environments, historical costs may not accurately reflect current market conditions or the actual cost structure.

- Complexity in Varied Product Lines: Companies with diverse product lines may find it challenging to apply a uniform accounting approach. Varying production processes and cost structures across different products can complicate cost analysis and decision-making.