What is cost of goods sold budget

A Cost of Goods Sold (COGS) budget is a financial plan that outlines anticipated expenses associated with producing goods or services over a specific period. It’s a forward-looking tool that helps businesses project and control costs related to production.

This budget typically includes raw materials, labor, and overhead costs. By estimating these expenses, companies can make informed decisions about pricing, production levels, and overall financial strategies.

Creating a COGS budget involves forecasting production needs, estimating associated costs, and aligning these projections with sales forecasts. It’s a crucial element in the broader budgeting process, providing insights into potential profitability and informing strategic financial planning.

A well-constructed COGS budget enables businesses to optimize resource allocation, set realistic revenue goals, and enhance overall financial performance. In essence, it’s a proactive financial roadmap that guides companies in navigating the intricacies of cost management within their production processes.

Understanding Cost of Goods Sold (COGS)

Cost of Goods Sold (COGS) is the total expense of making products or services. It covers raw materials, labor, and other production costs. To calculate COGS, subtract the ending inventory from the initial one. This helps businesses understand their production expenses. Lower COGS often means higher profits.

It’s a key factor for profit analysis and pricing strategies. Keeping COGS in check is crucial for financial success. In a nutshell, COGS is the cost directly tied to creating what a company sells. Monitoring and managing COGS is vital for effective financial decision-making in any business.

Significance of Cost of Goods Sold Budgeting

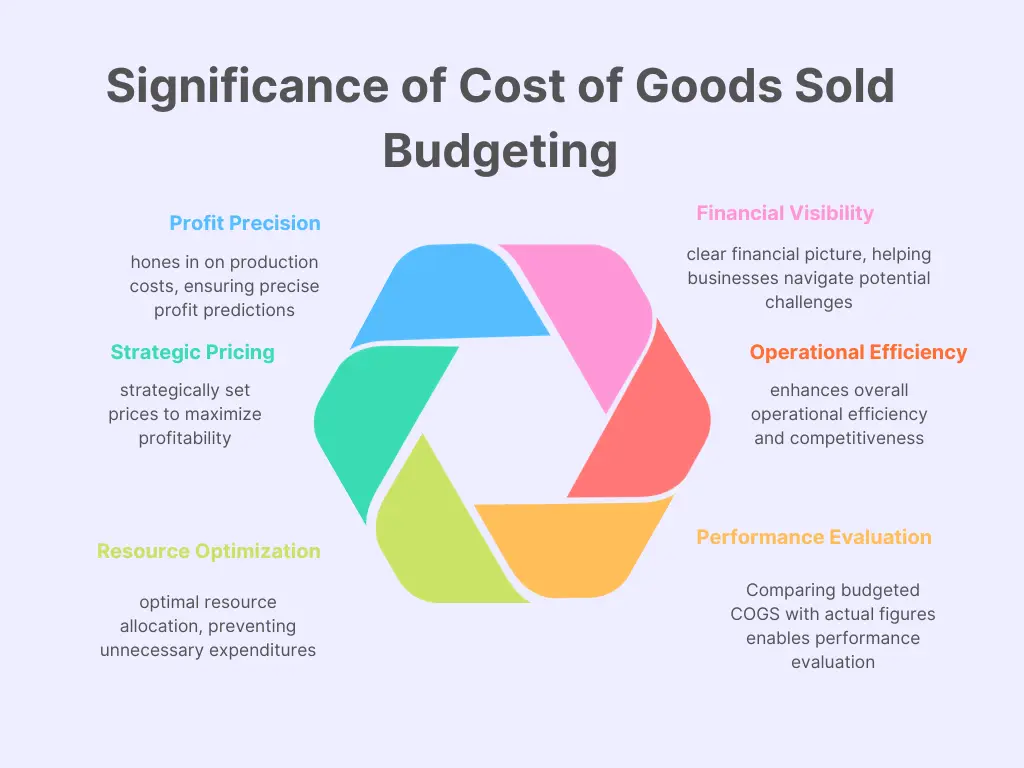

Profit Precision:

Cost of Goods Sold (COGS) budgeting hones in on production costs, ensuring precise profit predictions.

Strategic Pricing:

By anticipating expenses, businesses can strategically set prices to maximize profitability.

Resource Optimization:

Efficient budgeting aids in optimal resource allocation, preventing unnecessary expenditures.

Financial Visibility:

COGS budgeting offers a clear financial picture, helping businesses navigate potential challenges.

Operational Efficiency:

Streamlining production costs enhances overall operational efficiency and competitiveness.

Informed Decision-Making:

With a grasp on anticipated costs, businesses make informed decisions that impact their bottom line.

Performance Evaluation:

Comparing budgeted COGS with actual figures enables performance evaluation and adjustments.

Investor Confidence:

Transparent budgeting instills confidence in investors by showcasing sound financial management.

Crafting an Effective Cost of Goods Sold Budget

Define Scope:

Clearly outline the time frame and production scope the budget will cover, ensuring accuracy.

Collect Data:

Gather detailed information on raw materials, labor, and overhead costs involved in production.

Sales Forecast Integration:

Align the budget with sales forecasts to project production needs accurately.

Historical Analysis:

Examine past COGS data to identify trends, providing a foundation for realistic projections.

Cost Categorization:

Break down costs into categories, facilitating a granular understanding for better control.

Flexibility Consideration:

Incorporate flexibility to adapt to unforeseen changes, maintaining budget relevance.

Review and Adjust:

Regularly review actual costs against the budget, making necessary adjustments for precision.

Communication:

Ensure clear communication across departments for collaborative and informed decision-making.

Illustrative Case Study for COGS budget

In a manufacturing company, implementing a meticulous Cost of Goods Sold (COGS) budget proved instrumental in enhancing profitability. Let’s delve into the details:

Scenario:

The company, XYZ Manufacturing, experienced fluctuating profit margins due to inconsistent cost control. They decided to implement a comprehensive COGS budget for the upcoming fiscal year.

Steps Taken:

- Data Analysis:

- XYZ Manufacturing scrutinized historical data, revealing that raw material costs had increased by 15% annually.

- Sales Forecast Integration:

- Aligning the budget with a sales forecast, they predicted a 10% growth in demand for their products.

- Cost Projections:

- Anticipating increased demand, the company projected a 12% rise in production costs, factoring in both raw materials and labor.

Results:

The COGS budget forecasted a total production cost of $5 million for the fiscal year. With this insight, XYZ Manufacturing adjusted its pricing strategy, ensuring a profit margin of 20%.

Impact:

The meticulous COGS budgeting not only prevented potential losses but also allowed the company to secure a profit of $1 million. The proactive approach to cost management empowered XYZ Manufacturing to navigate market fluctuations while maintaining a competitive edge.

Conclusion:

This case study highlights how a well-crafted COGS budget, grounded in real data, can be a game-changer for companies, enabling them to optimize pricing strategies, ensure profitability, and fortify their financial standing in a dynamic market.

Wow, wonderful blog structure! How lengthy have you ever been blogging for?

you made running a blog glance easy. The whole glance of your site is fantastic,

let alone the content material! You can see similar: sklep internetowy and here sklep internetowy