Definition of Material Budget

Material budgeting is a strategic financial planning process that meticulously outlines the allocation, consumption, and procurement of resources within an organization. At its core, the material budget serves as a comprehensive blueprint, delineating the expected costs and quantities of materials essential for operational success.

This crucial component of financial management enables businesses to optimize resource utilization, minimize wastage, and enhance overall efficiency. In essence, the material budget is a proactive measure, of forecasting, and planning for the future demands of raw materials, components, and supplies. It involves a meticulous examination of historical consumption patterns, market dynamics, and production requirements to create a roadmap for effective resource management.

By providing a structured framework, it empowers organizations to make informed decisions, aligning material needs with strategic planning. Ultimately, it plays a pivotal role in promoting fiscal responsibility, operational resilience, and sustained financial excellence within the dynamic landscape of business operations.

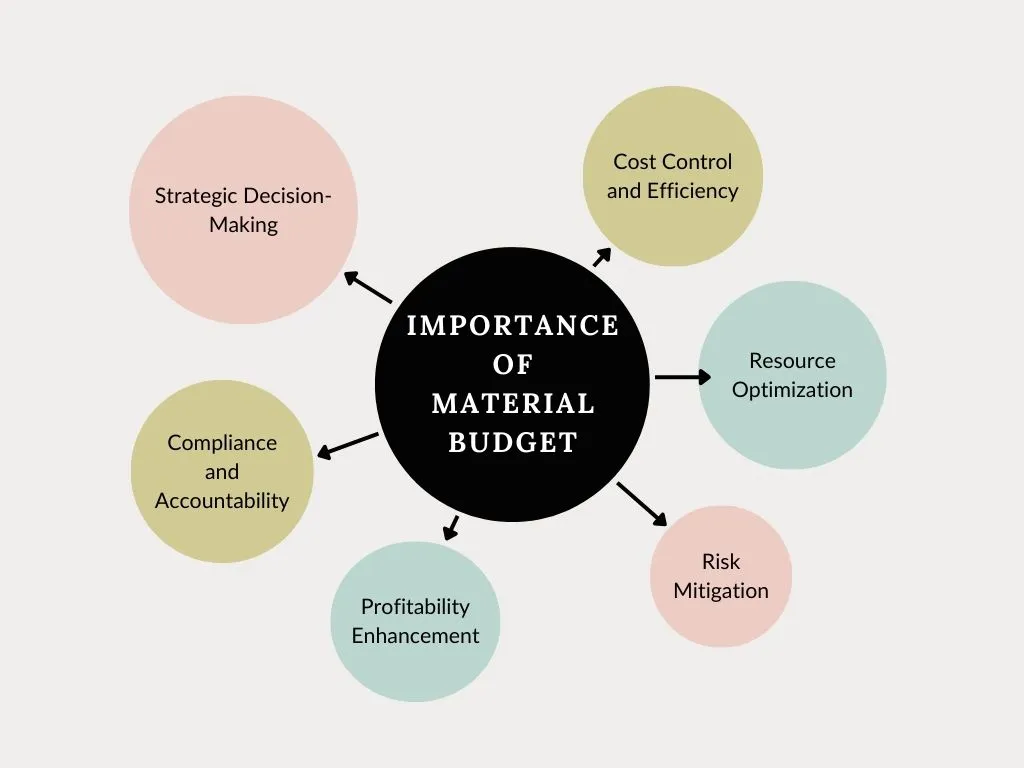

Significance and Impact in Financial Planning

Material budgeting holds paramount importance in the realm of financial planning, serving as a linchpin for strategic and sustainable fiscal management. Its relevance lies in its ability to align resource allocation with organizational objectives, fostering a streamlined and cost-effective operational environment.

Cost Control and Efficiency:

It enables meticulous control over costs associated with resource acquisition, consumption, and waste. By forecasting material needs, organizations can proactively identify cost control opportunities and enhance overall operational efficiency.

Resource Optimization:

Through a systematic analysis of historical consumption patterns and future requirements, material budgeting facilitates the optimization of resources. This ensures that the right quantities of materials are available at the right time, minimizing excess inventory and reducing carrying costs.

Strategic Decision-Making:

A well-constructed material budget serves as a foundation for informed decision-making. It provides insights into market trends, supplier performance, and production requirements, empowering financial planners to make strategic decisions that align with the organization’s goals.

Risk Mitigation:

Anticipating and planning for material shortages, price fluctuations, or supply chain disruptions is integral to risk mitigation. Material budgeting allows businesses to identify potential risks and implement contingency plans to maintain operational continuity.

Profitability Enhancement:

By effectively managing material costs, businesses can positively impact their bottom line. Material budgeting contributes to profit maximization by controlling expenses, improving resource utilization, and ensuring that financial resources are allocated judiciously.

Compliance and Accountability:

In a regulatory landscape, adherence to financial regulations and accountability are paramount. It establishes a framework for compliance by providing a transparent record of resource utilization, aiding in audits, and ensuring responsible financial practices.

Components of Material Budget

The components of a material budget are integral facets that collectively form a comprehensive framework for effective resource management within an organization:

- Material Identification: Precise recognition of the types and quantities of materials required for operational processes.

- Consumption Analysis: Thorough examination of historical consumption patterns to forecast future material needs accurately.

- Procurement Planning: Strategizing the acquisition of materials through efficient procurement processes, considering factors like pricing, vendor reliability, and supply chain dynamics.

- Inventory Management: Maintaining optimal inventory levels to prevent overstocking or stockouts, minimizing carrying costs and ensuring timely availability of materials.

- Cost Estimation: Accurately estimating the costs associated with acquiring, storing, and utilizing materials in various operational processes.

Calculating Material Budgets

Calculating material budgets is crucial for efficient production planning. Let’s take the example of making perfumes to illustrate this process. Suppose a perfume manufacturer aims to produce 1,000 bottles of a new fragrance. To determine the material budget, they need to consider the ingredients required for each bottle. If a bottle requires 50 milliliters of fragrance oil, 10 milliliters of alcohol, and 5 milliliters of water, the total material requirement would be 65 milliliters per bottle.

For 1,000 bottles:

- Fragrance oil needed = 50 ml/bottle * 1,000 bottles = 50,000 ml

- Alcohol needed = 10 ml/bottle * 1,000 bottles = 10,000 ml

- Water needed = 5 ml/bottle * 1,000 bottles = 5,000 ml

The material budget for this perfume batch would be 65,000 milliliters of ingredients. This calculation helps the manufacturer plan and procure the necessary materials, ensuring a smooth and cost-effective production process.

Material Consumption Budget

A Material Consumption Budget outlines the expected usage of raw materials in the production process. In the perfume industry, this budget projects the quantities and costs of essential components like fragrance compounds, alcohol, and packaging.

For instance, if ABC Perfumes plans to produce 10,000 units of a new scent, the Material Consumption Budget would estimate the required liters of essential oils, gallons of alcohol, and units of packaging materials. This proactive planning helps forecast expenses, streamline production, and ensure a seamless supply chain for optimal efficiency.

Materials Purchase Budget

Implementing the Material Consumption Budget, the Materials Purchase Budget details the procurement plan for acquiring the necessary raw materials. Continuing with the perfume manufacturing example, ABC Perfumes would specify the volume and cost of purchasing essential oils, alcohol, and packaging materials.

If essential oils cost $10 per liter and ABC Perfumes estimates the need for 500 liters, the Materials Purchase Budget would outline an allocation of $5,000 for essential oils. By aligning procurement with consumption estimates, this budget ensures timely material availability while controlling costs in the production cycle.

Practical Examples for Material Budgeting

| Material | Estimated Quantity | **Unit Cost ($) ** | **Total Cost ($) ** |

|---|---|---|---|

| Essential Oils | 500 liters | $10 | $5,000 |

| Alcohol | 300 gallons | $5 | $ 1,500 |

| Packaging Materials | 10,000 units | $2 | $ 20,000 |

| Material | Estimated Quantity | **Unit Cost ($) ** | **Total Cost ($) ** |

|---|---|---|---|

| Essential Oils | 500 liters | $10 | $5,000 |

| Alcohol | 300 gallons | $5 | $1,500 |

| Packaging Materials | 10,000 units | $2 | $20,000 |

Real industry example for material budgeting

In the automotive industry, Toyota employs robust material budgeting practices to optimize resource allocation. Through meticulous analysis of historical consumption patterns and market dynamics, Toyota forecasts the precise quantities and costs of raw materials required for vehicle production.

This strategic approach enables them to maintain efficient inventory levels, control costs, and enhance overall operational efficiency. Toyota’s material budgeting ensures a seamless supply chain, minimizes waste, and contributes to the company’s renowned production efficiency, exemplifying the strategic importance of material budgeting in sustaining competitiveness within the automotive sector.

Recapitulation of Key Concepts

Material budgeting is a strategic financial planning process crucial for resource optimization within organizations. Serving as a comprehensive blueprint, it outlines the allocation, consumption, and procurement of materials, ensuring operational success.

This financial management component allows businesses to forecast and plan for future material demands, minimizing wastage, and enhancing efficiency. Key elements include cost control, resource optimization, strategic decision-making, risk mitigation, profitability enhancement, compliance, and accountability.

Wow, marvelous blog structure! How lengthy have you ever been blogging for?

you made blogging look easy. The entire glance of your website is excellent, let alone

the content material! You can see similar: sklep online and here sklep internetowy

magnificent issues altogether, you simply gained a emblem new

reader. What might you suggest about your publish that you

made some days ago? Any sure?

2D explainer video company in India Video Company India

https://en-web-directory.com/listings12705641/explainer-video-company-india

https://www.managingmadrid.com//users/explainer_video_company_india