What is ABC analysis?

ABC analysis is a widely used inventory management technique that classifies items into three categories based on their relative importance and value. This analysis considers the Pareto principle, which states that a small percentage of items typically account for the majority of the total value or impact.

ABC analysis categorizes items as A, B, or C, with A representing the most critical items and C representing the least critical ones. The criteria for categorizing items include stock value, sales volume, revenue generation, profitability, and demand frequency.

The purpose of ABC analysis is to allocate resources efficiently and prioritize inventory management efforts. Classifying items allows organizations to focus their attention and resources on the items that have the highest impact on their operations. It helps identify high-value items that require close monitoring, while also highlighting low-value items that may not warrant extensive management efforts.

By segmenting inventory in this way, organizations can optimize inventory control, reduce carrying costs, improve customer service, and make more informed decisions regarding procurement, production, and distribution.

Categories of ABC analysis

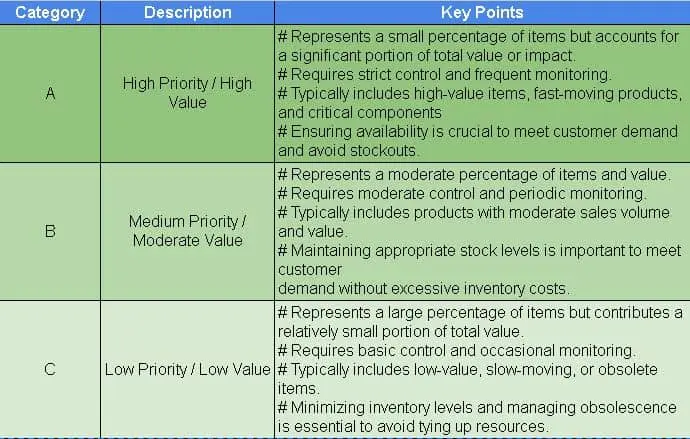

Category A:

This category represents the most important and valuable items. These items typically have a high sales volume, generate a significant portion of revenue, or contribute significantly to profitability. Category A items are often characterized by high demand frequency and require close monitoring and tight inventory control to ensure their availability.

Category B:

This category includes items that have moderate importance and value, have a moderate sales volume, and contribute to revenue and profitability to a lesser extent than Category A items. Category B items require a moderate level of attention and inventory management effort.

Category C:

This category comprises items with the lowest importance and value. They have a relatively low sales volume, contribute minimally to revenue and profitability, and often have sporadic demand. Category C items require minimal management efforts and can be handled with less scrutiny and inventory control.

Step-by-step procedures for conducting ABC analysis

- Gather data: Collect information on items, such as sales volume, revenue, or profitability, to determine their importance and value.

- Calculate item metrics: Calculate relevant metrics for each item, such as percentage contribution to total value or frequency of demand.

- Rank items: Assign higher ranks to items with greater importance or value by sorting them in descending order.

- Determine categorization thresholds: Set thresholds to divide the ranked items into A, B, and C categories based on the desired proportion or value contribution.

- Categorize items: Assign each item to the appropriate category based on its rank and the predefined thresholds.

- Review and adjust: Review the categorization results and make any necessary adjustments based on business-specific considerations or expert judgment.

Uses of ABC analysis

Inventory optimization:

ABC analysis helps optimize inventory levels by focusing resources on high-value items (Category A) and reducing excessive inventory for low-value items (Category C).

Demand forecasting:

By understanding the demand patterns of different item categories, ABC analysis assists in accurate demand forecasting and aligning production and procurement activities accordingly.

Supplier management:

Businesses can prioritize suppliers based on their performance and the importance of the items they provide, allowing them to build strong relationships.

Cost control:

By identifying high-value items (Category A), businesses can allocate resources effectively, negotiate better pricing, and implement cost-saving measures.

Risk management:

ABC analysis enables businesses to identify critical items (Category A) that may pose higher risks, such as supply disruptions, and implement contingency plans to mitigate those risks.

Benefits of ABC analysis

Improved resource allocation:

By categorizing items based on their importance and value, ABC analysis helps allocate resources more efficiently. It ensures that critical items (Category A) receive appropriate attention and resources while avoiding overinvestment in less important items (Category C).

Optimal inventory management:

ABC analysis enables businesses to prioritize inventory control efforts. It helps maintain optimal stock levels for high-value items (Category A) to prevent stockouts while reducing inventory and carrying costs for low-value items (Category C).

Enhanced decision-making:

With ABC analysis, businesses gain a clearer understanding of their inventory composition and can make informed decisions regarding procurement, production, distribution, and pricing strategies based on the importance and value of items in each category.

Improved customer service:

By focusing on high-priority items (Category A), businesses can ensure better availability and responsiveness to customer demands, resulting in improved customer satisfaction and loyalty.

Cost savings:

ABC analysis helps identify cost-saving opportunities by identifying areas where excessive inventory or inefficient resource allocation can be reduced, leading to lower carrying costs and improved profitability.

Limitations of ABC analysis

Subjectivity in categorization:

Setting thresholds and assigning items to categories can be subjective and may vary based on individual judgment or business-specific criteria.

Lack of consideration for variability:

ABC analysis often focuses solely on value or importance, overlooking factors such as demand variability, lead time, or supply chain risks that can impact inventory management.

Static nature:

ABC analysis assumes that item categorizations remain constant over time, while in reality, item characteristics and market conditions may change, requiring periodic reevaluation.

Ignores interdependencies:

ABC analysis treats items independently, disregarding potential interdependencies or relationships between items that could influence their categorization and management.

It is important to consider these limitations and supplement ABC analysis with other techniques and considerations for a comprehensive and robust inventory management strategy.

[…] ABC Analysis: Prioritize items based on their importance, categorizing them as A, B, or C items according to their value and impact on production. […]