Activity Based Costing (ABC) is a modern cost accounting system that provides a more accurate and detailed analysis of how costs are incurred within the organization. Traditional costing methods often allocate costs based on simple metrics like direct labor hours or machine usage, which can lead to distorted cost calculations and misinformed decision-making. ABC is one of the modern approaches to manufacturing accounting.

The ABC assigns costs to specific activities or processes that contribute to the production of goods or services. It recognizes that various activities consume resources and drive costs, regardless of the volume of output. By identifying and allocating costs based on these activities, ABC helps organizations to better understand the true costs related to their products, services, or processes.

ABC follows a step-by-step methodology that involves identifying activities, determining cost drivers, and assigning costs to cost drivers. It provides a more comprehensive view of cost allocation by considering both direct costs (easily traceable to specific activities) and indirect costs (shared among multiple activities).

Advantages of activity based costing

Activity Based Costing (ABC) has several advantages over traditional costing methods. Here are some key advantages of Activity Based Costing.

- Enhanced Cost Accuracy: ABC provides a more accurate and precise allocation of costs by directly linking them to specific cost drivers. This eliminates the arbitrary allocation of indirect costs and provides a more realistic view of the resources consumed by each activity. As a result, the cost information obtained through ABC is more reliable for decision-making.

- Improved Cost Visibility: ABC offers greater transparency by breaking down costs into various activities. This allows organizations to identify the cost drivers and understand how resources are utilized at each level of their operations. It enables a better understanding of the true costs associated with products, services, or processes, facilitating more informed pricing decisions.

- Effective Resource Allocation: By identifying the activities that drive costs, ABC helps organizations allocate resources more effectively. It enables management to focus on activities that provide the most value and eliminate or streamline non-value-added activities. This leads to improved efficiency and reduced wastage of resources.

- Accurate Product/Service Profitability Analysis: ABC enables organizations to determine the profitability of individual products, services, or customer segments more accurately. By assigning costs based on the activities required to produce or deliver them, ABC provides insights into the true costs associated with each offering. This information can guide pricing strategies and help identify areas for cost reduction or value enhancement.

- Facilitates Process Improvement: With its detailed cost analysis, ABC helps identify bottlenecks and inefficiencies within processes. By understanding the costs and resource utilization at each activity level, organizations can target areas for improvement. This information aids in making process modifications, optimizing workflows, and enhancing overall operational efficiency.

How activity-based costing works

Activity Based Costing (ABC) works by breaking down an organization’s costs into specific activities and allocating those costs based on the resources consumed by each activity. The process begins with identifying the activities involved in producing goods or delivering services. Next, cost drivers are determined, which are the factors that cause costs to be incurred within each activity. These cost drivers can be different for each activity and may include measures such as labor hours, machine usage, or the number of setups.

Once the cost drivers are established, costs are allocated to each activity based on their respective consumption of resources. Finally, the costs allocated to activities are assigned to products, services, or customer segments based on the proportionate usage of those activities. This enables a more accurate calculation of the true costs associated with each output and provides insights into resource utilization and profitability.

Basic requirements of ABC

- Identification of Activities: The first requirement is to identify and define the activities involved in the production process or service delivery. This involves breaking down the overall operations into distinct activities that consume resources.

- Determination of Cost Drivers: Each activity needs to have a corresponding cost driver, which is a factor that causes costs to be incurred within that activity. Cost drivers can be based on factors such as time, volume, complexity, or any other appropriate measure that accurately reflects the consumption of resources.

- Measurement of Resource Consumption: The next step is to measure the consumption of resources for each activity. This includes tracking the usage of labor, materials, equipment, utilities, and any other resources associated with the activity.

- Allocation of Costs: Once the resource consumption is measured, the costs need to be allocated to each activity based on the usage of resources. This involves assigning the appropriate cost to each activity in proportion to its resource consumption.

- Assignment of Costs to Outputs: Finally, the costs allocated to activities are assigned to the final outputs, such as products, services, or customer segments. This step involves determining the proportionate usage of activities by each output and assigning the respective costs accordingly.

Activity based costing- a practical example

Here’s an example of Activity Based Costing (ABC) for a manufacturing company, XYZ

Identify Activities:

XYZ Manufacturing identifies three key activities involved in its production process:

- Material procurement

- Machine setup

- Assembly

Determine Cost Drivers:

For each activity, XYZ Manufacturing determines the appropriate cost driver.

- For material procurement, the cost driver could be the number of purchase orders placed.

- Machine setup, the cost driver could be the number of setups required.

- Assembly, the cost driver could be the number of units produced.

| Activity | Cost drivers |

| Material procurement | Number of purchase orders |

| Machine setup | Number of setups |

| Assembly | Number of units produced |

- Measure Resource Consumption: XYZ Manufacturing tracks the resources consumed for each activity. Let’s consider the following resource consumption for each activity:

- Material Procurement: Total annual cost = $500,000

- Number of purchase orders placed = 500

- Machine Setup: Total annual cost = $300,000

- Number of setups required = 200

- Assembly: Total annual cost = $1,000,000

- Number of units produced = 10,000

Allocate Costs to Activities: XYZ Manufacturing allocates the costs incurred for each activity based on the respective cost drivers. Let’s calculate the cost allocation per unit for each activity.

- Material Procurement: Cost per purchase order = $500,000 / 500 = $1,000 per purchase order.

- Machine Setup: Cost per setup = $300,000 / 200 = $1,500 per setup.

- Assembly: Cost per unit = $1,000,000 / 10,000 = $100 per unit.

Assign Costs to Products:

Finally, XYZ Manufacturing assigns the costs from each activity to its products based on their respective usage.

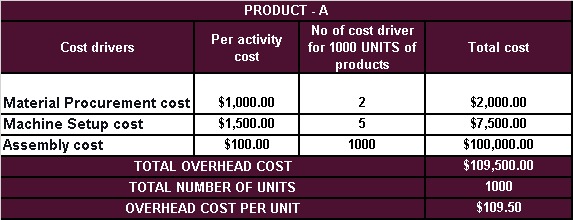

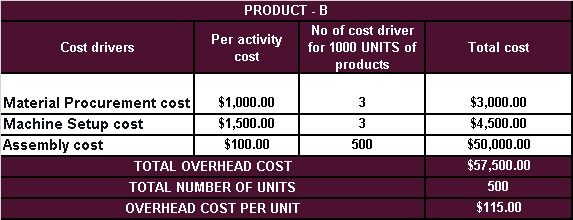

Let’s assume Product A requires 2 purchase orders, 5 setups, and produces 1,000 units, while Product B requires 3 purchase orders, 3 setups, and produces 500 units. The cost allocation for each product would be:

Product A:

Product B:

By implementing ABC, XYZ Manufacturing can accurately allocate costs to each product based on its specific activities and usage. This information can assist in pricing decisions, product profitability analysis, and identifying opportunities for cost optimization and process improvement within manufacturing operations.

Limitations of activity based costing

- Time and Cost Intensive:

Implementing ABC requires significant time, effort, and resources. It involves identifying activities, determining cost drivers, collecting data, and setting up a complex cost allocation system. This can be burdensome and costly, especially for small or resource-limited organizations.

- Subjectivity in Cost Driver Selection:

Selecting the most appropriate cost drivers for activities often involves subjective judgment. Different individuals or teams may have varying opinions on which cost drivers are most relevant, leading to potential bias or inconsistency in cost allocations.

- Complex Data Requirements:

ABC relies on detailed and accurate data regarding resource consumption and activity costs. Gathering this data can be challenging, as it may require tracking and monitoring numerous cost drivers and activity inputs. Organizations with limited data systems or poor data quality may struggle to implement ABC effectively.

- Difficulty in Maintaining Relevance:

Over time, activities, processes, and cost drivers may change due to factors such as technology advancements, market shifts, or process improvements. This dynamic nature of business operations makes it challenging to continuously update and maintain the relevance of ABC systems.

- Potential Overhead Allocation Issues:

ABC emphasizes the allocation of indirect costs to activities, which can lead to complexities in allocating overhead costs accurately. It requires careful consideration and judgment to determine the appropriate allocation of indirect costs, and there is a risk of subjective interpretations or misallocation.

- Limited Strategic Insights:

While ABC provides detailed cost information at the activity level, it may not offer comprehensive strategic insights on factors such as pricing, market positioning, or competitive advantage.

- Resistance to Change:

Implementing ABC may face resistance from employees, particularly if it results in changes to existing cost allocation methods or performance evaluation systems. Employees may find it challenging to adapt to a new cost measurement approach, leading to potential resistance and decreased acceptance.

[…] Activity-Based Costing (ABC) is a costing methodology used by manufacturers to allocate costs more accurately by linking them to specific activities within the organization. ABC recognizes that not all activities consume resources in the same way and aims to assign costs based on the actual consumption of resources by each activity. This method involves identifying various activities involved in the production process and determining their cost drivers, such as machine hours, setups, or orders. […]

[…] Cost Reduction: Production planning enables organizations to identify cost-saving opportunities. By streamlining production processes, minimizing idle time, and eliminating unnecessary inventory, businesses can reduce operational costs and enhance profitability. It enables the implementaion of activity based costing. […]

[…] Activity-Based Costing (ABC) is a costing method that allocates costs to specific activities or cost drivers based on their consumption of products or services. Unlike traditional costing methods that rely on volume-based allocation, ABC takes into account the complexity and diversity of activities involved in the production process. It helps identify the cost drivers that directly influence the consumption of resources, providing a more accurate and detailed picture of the cost structure. […]

[…] Activity-Based Costing (ABC) is an alternative method for allocating overhead expenses that focuses on activities performed within an organization. ABC identifies the specific activities that consume resources and assigns costs based on the extent of their utilization. It recognizes that not all products or services consume overhead resources in the same way. […]

[…] Activity-based costing (ABC) is a costing method that aims to allocate overhead costs more accurately by identifying and assigning costs to specific activities within an organization. Unlike the traditional costing method, which relies on broad cost drivers, ABC focuses on the activities that consume resources. It involves analyzing the activities performed, determining their cost drivers, and allocating overhead based on the usage of these drivers. ABC provides a more detailed and precise understanding of cost behavior, enabling businesses to make informed decisions about pricing, process improvement, and resource allocation. […]